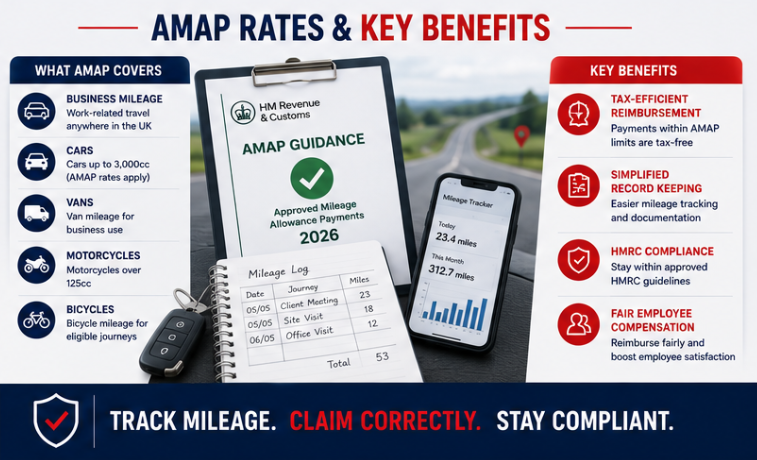

The AMAP rate 2026 update is the most significant mileage change in fifteen years. From 6 April 2026, HMRC increased the Approved Mileage Allowance Payment rate for cars and vans from 45p to 55p per mile for the first 10,000 business miles in a tax year. Beyond 10,000 miles, the rate remains at 25p per mile.

Still, this change affects your payroll, your expenditure policy, If your business reimburses workers for using their own vehicles. Then’s what you need to understand.

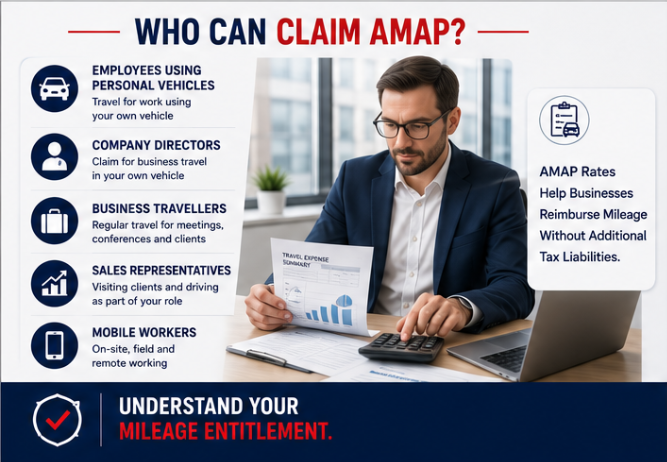

What Is the AMAP Rate and Why Does It Matter

When workers drive their personal car for job tasks, companies can pay them back without taxing it – the amount follows a standard set by HMRC. This figure decides exactly how much of that travel cost stays free from tax.

When reimbursement stays within the set limit, the worker faces no extra tax and nothing shows up as a perk. Go past that limit, however, then the surplus counts as taxable pay, something HMRC wants listed on form P11D.

The AMAP rate 2026 increase to 55p means employers can now reimburse up to 55p per mile for the first 10,000 business miles without triggering an income tax charge or a P11D obligation.

What Changed on 6 April 2026

The previous rate of 45p had been in place since 2011. The Spring Statement 2025 confirmed the increase to 55p, effective from the start of the 2026/27 tax year, 6 April 2026.

The rates for motorcycles and bikes were n’t changed. Motorcycles remain at 24p per mile. Bikes remain at 20p per mile.

This is a straightforward change to HMRC’s approved rates. Employers are not required to pay 55p; the AMAP rate is a ceiling for tax-free reimbursement, not a legal minimum. Many employers choose to pay below the approved rate.

The Income Tax and NIC Position: What HMRC Has Said

This is the area where employers need to pay close attention and take proper advice.

HMRC has acknowledged publicly that the income tax rules and the National Insurance Contributions rules for mileage payments do not always move in lockstep. When a rate change is made to the AMAP rate, the NIC position may be governed by separate legislation and may not automatically update at the same time.

This means there can be a period where the income tax treatment and the NIC treatment of mileage payments differ. The specific position for the AMAP rate 2026 increase and what it means for the employer and employee NIC is something HMRC has been asked to clarify.

This is precisely why you shouldn’t rely on general information alone. The NIC rules are specialized, and the consequences of getting payroll treatment wrong can include penalties, interest, and backdated arrears. Speak to a good duty counsel before streamlining your payroll rate or making opinions about payment structure.

Three Situations Worth Reviewing

You Are Currently Paying 45p Per Mile

If you have not yet updated your mileage rate to reflect the AMAP rate 2026 increase, your employees are being reimbursed below the current approved rate. They may be entitled to claim Mileage Allowance Relief on the shortfall, which is the difference between what you paid and the approved 55p rate.

Employees claim this through Self Assessment if they file a return, or through a P87 form if they do not. For someone driving 8,000 business miles reimbursed at 45p, the shortfall is 10p per mile, £800 in unclaimed relief. At the basic rate of income tax, that is £160, they could claim back.

You Have Already Updated to 55p Per Mile

Good, your employees are being reimbursed at the approved rate, so there is no income tax or P11D issue on the mileage payments themselves. But as noted above, review the NIC position with your adviser before assuming the picture is entirely clean.

Also, check whether the change needs to be applied from 6 April 2026. Still, workers who drove business long hauls before in the time at the old rate may be owed a top- up for those peregrinations, if you streamlined your policy part- way through the duty time.

You Pay a Car Allowance and a Low Mileage Rate

Some employers pay a monthly car allowance as part of salary, then reimburse mileage at a rate below the AMAP rate, for example, 20p or 30p per mile. The car allowance is treated as earnings for PAYE and NIC purposes.

In this type of arrangement, employees may be able to claim Mileage Allowance Relief on the gap between what they received in mileage payments and the approved AMAP rate. The tax treatment of the car allowance itself is a separate question. If you run this kind of structure, it is worth a proper review to make sure both the employer and employee positions are correct.

What Employers Should Do Now

Update your expenditure and avail policy. However, update it to reflect the new approved rate. If your written policy still references 45p. Make clear to workers what rate you’ll pay and from what date.

Check your payroll software. Systems running on Xero, Sage, or QuickBooks should be updated to reflect the new rate. Do not assume the software has automatically verified the figure in your settings.

Review mileage records from 6 April 2026 onwards. If you have not yet applied the new rate retroactively, pull your mileage records from the start of the tax year and assess whether a top-up is needed.

Don’t ignore the NIC question. Get specific advice from a good duty professional on how the AMAP rate 2026 increase affects your National Insurance position. This isn’t commodity general guidance that can resolve for your specific payroll setup.

What Employees Can Claim

If your employer pays below the AMAP rate 2026 approved rate, you are entitled to claim Mileage Allowance Relief on the difference. This is a legitimate tax relief available through HMRC; it is not a grey area.

To make a claim, you need accurate avail records. HMRC expects a log that includes the date of each trip, the launch and end point, the business purpose, and the number of long hauls driven. A simple spreadsheet works. So does a mileage tracking app. What does not work is a rough estimate put together at the end of the year.

If you have already filed a Self Assessment return, you claim Mileage Allowance Relief in your return. If you do not file a return, use form P87 available on GOV. UK to claim directly from HMRC. You can claim for the current tax year and up to four previous tax years where records exist.

A Note for Owner-Directors of Limited Companies

Still, the AMAP rate 2026 change is applicable to both your pot duty deduction and your payroll treatment. If you operate through a limited company and repay yourself for business expenses.

Mileage reimbursements at or below the approved rate are a deductible business expense, the company gets a corporation tax deduction, and you do not pay income tax or NIC on the reimbursement. That makes mileage claims one of the most tax-efficient ways to extract value from a limited company for genuine business travel.

Keep your mileage records properly. HMRC does scrutinize mileage claims during compliance checks, and a limited company director with no log to show is in a weak position. Your accountant can help you set up a simple process that satisfies HMRC without taking hours of your time.

Act Before the Tax Year Gets Away From You

The AMAP rate 2026 increase is a practical change that touches payroll, expenditure policy, Self Assessment, and potentially NIC all at once. The utmost of it’s manageable with a clear process and the right advice.

The part that catches businesses out isn’t the rate change itself. It’s the supposition that streamlining a number in a payroll system is all that’s demanded. A proper review looks at your full available payment structure, your NIC position, your P11D scores, and your hand dispatches, not just the pence-per-farthing.

At Tax Consultant UK, we help employers, directors, sole traders, and employees get their tax positions right, whether that means a payroll review, a Self Assessment claim, or a compliance check ahead of an HMRC query. We work with businesses across West Yorkshire, London, Manchester, and Bristol, and our advice is straightforward and specific to your situation.

Get in touch with Tax Consultant UK today. Use the contact form, call our office, or send us a message, and we will give you a clear, honest answer on where you stand with the new mileage rules.